1. OUR OPINION IS UNMODIFIED

We have audited the financial statements of Severfield plc (“the Company”) for the 52-week period ended 25 March 2023 which comprise the Consolidated income statement, Consolidated statement of comprehensive income, Consolidated balance sheet, Consolidated statement of changes in equity, Consolidated cash flow statement, Company balance sheet, Company statement of changes in equity, and the related notes, including the accounting policies in note 1.

In our opinion:

the financial statements give a true and fair view of the state of the Group’s and of the parent Company’s affairs as at 25 March 2023 and of the Group’s profit for the year then ended;

the Group financial statements have been properly prepared in accordance with UK-adopted international accounting standards;

the parent Company financial statements have been properly prepared in accordance with UK accounting standards, including FRS 101 Reduced Disclosure Framework and as applied in accordance with the provisions of the Companies Act 2006; and

the financial statements have been prepared in accordance with the requirements of the Companies Act 2006.

Basis for opinion

We conducted our audit in accordance with International Standards on Auditing (UK) (“ISAs (UK)”) and applicable law. Our responsibilities are described below. We believe that the audit evidence we have obtained is a sufficient and appropriate basis for our opinion. Our audit opinion is consistent with our report to the audit committee.

We were first appointed as auditor by the shareholders on 2 September 2015. The period of total uninterrupted engagement is for the eight financial periods ended 25 March 2023. We have fulfilled our ethical responsibilities under, and we remain independent of the Group in accordance with, UK ethical requirements including the FRC Ethical Standard as applied to listed public interest entities. No non-audit services prohibited by that standard were provided.

| Overview |

| Materiality: Group financial statements as a whole | £1.4m (2022: £1.4m) 5.1% (2022: 4.9%) of profit before tax (2022: adjusted profit before tax) |

| Coverage | 97% (2022: 98%) of group profit before tax* |

| Key audit matters | vs 2022 |

| Recurring risk | Carrying value of construction contract assets, and revenue and profit recognition in relation to construction contracts | |

| Parent Company’s Key audit matter: Carrying value of parent Company’s investments in subsidiaries and joint ventures, and recoverability of intercompany debtors | |

* This is the profit and losses as a percentage of total profits and losses that made up the group profit before tax.

2. Key audit matters: our assessment of risks of material misstatement

Key audit matters are those matters that, in our professional judgement, were of most significance in the audit of the financial statements and include the most significant assessed risks of material misstatement (whether or not due to fraud) identified by us, including those which had the greatest effect on: the overall audit strategy; the allocation of resources in the audit; and directing the efforts of the engagement team. We summarise below the key audit matters (unchanged from 2022), in decreasing order of audit significance, in arriving at our audit opinion above, together with our key audit procedures to address those matters and, as required for public interest entities, our results from those procedures. These matters were addressed, and our results are based on procedures undertaken, in the context of, and solely for the purpose of, our audit of the financial statements as a whole, and in forming our opinion thereon, and consequently are incidental to that opinion, and we do not provide a separate opinion on these matters.

| The risk | Our response |

Carrying value of construction contract assets, and revenue and profit recognition in relation to construction contracts

Revenue:

£491.8m (2022: £403.6m)

Contract Asset:

£48.8m (2022: £74.9m)

Refer to Audit Committee Report, (Note 1) and note 18 (financial disclosures). | Subjective estimate

The Group’s activities are undertaken via long-term construction contracts.

The carrying value of the construction contract assets, as well as the revenue and profit recognised, are based on an input measure (being costs incurred to date as a proportion of estimated total contract costs) and estimates of total contract consideration (being agreed contract consideration plus elements of variable consideration such as instances where the value of contract modifications is currently unagreed).

Estimated total contract costs, and as a result revenues, can be affected by a variety of uncertainties that depend on the outcome of future events resulting in revisions throughout the contract period.v

The effect of these matters is that, as part of our risk assessment for audit planning purposes, we determined that the carrying value of contract assets, revenue and profit recognised on construction contracts has a high degree of estimation uncertainty, with a potential range of reasonable outcomes greater than our materiality for the financial statements as a whole, and possibly many times that amount. Therefore, auditor judgement is required to assess whether the directors’ estimates for total forecast costs and variable consideration falls within an acceptable range. The financial statements (note 2) disclose the nature and extent of the estimates and judgements made by the Group. | We performed the tests below rather than seeking to rely on any of the Company’s controls because the nature of the balance is such that we would expect to obtain audit evidence primarily through the detailed procedures described.

Our procedures included:

- Our sector experience: Identifying high risk contracts with risk indicators including: large carrying value of contract assets, low margin or loss-making contracts with significant costs to complete estimates, uncertainty over variable consideration, and large contracts with significant costs to complete;

- Tests of detail: For the high risk contracts identified, assessing management’s judgement that revenue recognised is highly probable to not be reversed by agreeing to post period-end revenue certification, customer variation agreement or cash;

- Our sector experience: Assessing forecasted costs to complete in the sample of high risk contracts identified by understanding contract performance and costs incurred post period-end, along with discussion and challenge of management’s costs to complete estimates against original budgets, current run rates and known risks;

- Tests of detail: Assessing the accuracy of costs incurred to date through sample testing, including an assessment of whether the cost sampled was allocated to the appropriate contract;

- Historical comparisons: Assessing the forecasting accuracy of contract revenue and costs by evaluating initial forecasted margins for a sample of contracts across the portfolio against actual margins achieved;

- Site visits: For certain higher risk or larger value contracts, attending in person site visits, with the involvement of our own industry specialists for a sample of these, inspecting the physical progress on site for individual projects and identifying areas of complexity through observation and discussion with site personnel;

- KPMG specialists: For certain higher risk or larger contracts, utilising KPMG Project specialists to identify the risks and opportunities associated with the contract and develop a range of possible contract out-turns and challenge the appropriateness of revenue recognised and provisions held in relation to these contracts;

- Assessing transparency: Assessing the adequacy of the Group’s disclosures on revenue recognition and the degree of estimation involved in arriving at the construction contract assets and associated revenue and profit recognition.

Our results:

- We found the carrying value of construction contract assets, and the level of revenue and profit recognition in relation to construction contracts, to be acceptable (2022: acceptable).

|

| The risk | Our response |

Carrying value of parent Company’s investments in subsidiaries and joint ventures, and recoverability of inter-company debtors

Investments:

£152.6m (2022: £152.6m)

Intercompany receivables:

£105.6m (2022: £69.0m)

Refer to (Note 1) and (Note 4). | Low risk, high value

The carrying amount of the parent Company’s investments in subsidiaries and joint ventures, and the intra-group debtor balances represent 46% (2022: 52%) and 32% (2022: 24%) of the Company’s total assets respectively. Their recoverability is not at a high risk of significant misstatement or subject to significant judgement. However, due to their materiality in the context of the parent Company financial statements, this is considered to be the area that had the greatest effect on our overall parent Company audit. | We performed the tests below rather than seeking to rely on any of the Company’s controls because the nature of the balance is such that we would expect to obtain audit evidence primarily through the detailed procedures described.

Our procedures included:

- Tests of detail: Comparing the carrying amount of 100% of the investments balance with the relevant subsidiaries’ and joint ventures’ draft balance sheets to identify whether their net assets, being an approximation of their minimum recoverable amount, were in excess of their carrying amount and assessing whether those subsidiaries and joint ventures have historically been profit making.

- Tests of detail: Assessing 100% of the total group debtors balance to identify, with reference to the relevant debtors’ draft balance sheet, whether they have a positive net asset value and therefore coverage of the debt owed, as well as assessing whether those debtor companies have historically been profit-making.

- Our sector experience: For the investments where the carrying amount exceeded the net asset value, comparing the carrying amount of the investment with the expected value of the business based on a suitable multiple of the subsidiaries’ and joint ventures’ profit.

Our results:

- We found the Company’s conclusion that there is no impairment of its investments in subsidiaries, joint ventures and intercompany debtors to be acceptable (2022: acceptable).

|

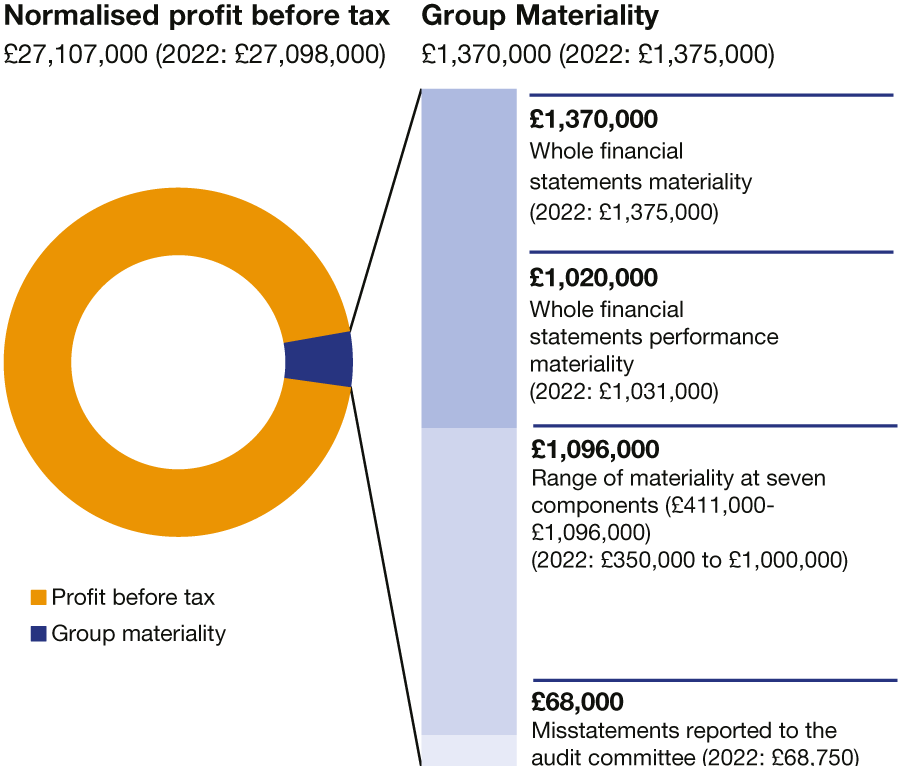

3. Our application of materiality and an overview of the scope of our audit

Materiality for the Group financial statements as a whole was set at £1,370,000 (2022: £1,375,000), determined with reference to a benchmark of Group’s profit before tax (2022: normalised to exclude amortisation and costs as a result of acquisitions as disclosed in note 5) of which it represents 5.1% (2022: 4.9%)

Materiality for the parent Company financial statements as a whole was set at £959,000 (2022: £900,000), determined with reference to a benchmark of Company’s total assets, of which it represents 0.3% (2022: 0.3%).

In line with our audit methodology, our procedures on individual account balances and disclosures were performed to a lower threshold, performance materiality, so as to reduce to an acceptable level the risk that individually immaterial misstatements in individual account balances add up to a material amount across the financial statements as a whole.

Performance materiality was set at 75% (2022: 75%) of materiality for the financial statements as a whole, which equates to £1,020,000 (2022: £1,031,000) for the Group and £719,000 (2022: £750,000) for the parent Company. We applied this percentage in our determination of performance materiality because we did not identify any factors indicating an elevated level of risk.

We agreed to report to the Audit Committee any corrected or uncorrected identified misstatements exceeding £68,000 (2022: £68,750), in addition to other identified misstatements that warranted reporting on qualitative grounds.

Of the Group’s 15 (2022: 16) reporting components, we subjected 7 (2022: 7) to full scope audits for group purposes.

The components within the scope of our work accounted for the percentages illustrated opposite.

The remaining 5% (2022: 7%) of total Group revenue, 3% (2022: 2%) of Group profit before tax and 4% (2022: 4%) of total Group assets is represented by 8 (2022: 9) reporting components, none of which individually represented more than 4% (2022: 3%) of any of total Group revenue, Group profit before tax or total Group assets. For these components, we performed analysis at an aggregated group level to re-examine our assessment that there were no significant risks of material misstatement within these.

The Group team instructed component auditors as to the significant areas to be covered, including the relevant risks detailed above and the information to be reported back.

The Group team set the component materialities, which ranged from £411,000 to £1,096,000 (2022: £350,000 to £1,000,000) having regard to the mix of size and risk profile of the Group across the components.

The work on one of the seven components (2022: one of the seven components) was performed by component auditors and the rest, including the audit of the parent Company, was performed by the Group team.

The Group team visited 1 (2022: 0) component locations in India (2022: India) to assess the audit risk and strategy. Video and telephone conference meetings were also held with the component auditors. At these visits and meetings, the findings reported to the Group team were discussed in more detail, and any further work required by the Group team was then performed by the component auditor. The Group team also reviewed the audit file of the component auditor.

4. Going Concern

The directors have prepared the financial statements on the going concern basis as they do not intend to liquidate the Group or the Company or to cease their operations, and as they have concluded that the Group's and the Company's financial position means that this is realistic. They have also concluded that there are no material uncertainties that could have cast significant doubt over their ability to continue as a going concern for at least a year from the date of approval of the financial statements ("the going concern period").

We used our knowledge of the Group, its industry, and the general economic environment to identify the inherent risks to its business model and analysed how those risks might affect the Group's and Company's financial resources or ability to continue operations over the going concern period. The risks that we considered most likely to adversely affect the Group's and Company's available financial resources and metrics relevant to debt covenants over this period were:

ongoing economic issues including inflationary pressures and the resulting challenging market.

the potential for contract assets to increase as a result of contractual disputes or operational difficulties, leading to an increased working capital requirement.

Our conclusions based on this work:

we consider that the directors' use of the going concern basis of accounting in the preparation of the financial statements is appropriate;

we have not identified, and concur with the directors' assessment that there is not, a material uncertainty related to events or conditions that, individually or collectively, may cast significant doubt on the Group's or Company's ability to continue as a going concern for the going concern period;

we have nothing material to add or draw attention to in relation to the directors' statement in note 1 to the financial statements on the use of the going concern basis of accounting with no material uncertainties that may cast significant doubt over the Group and Company's use of that basis for the going concern period, and we found the going concern disclosure in note 1 to be acceptable; and

the related statement under the Listing Rules set out on Our Financial Performance is materially consistent with the financial statements and our audit knowledge.

However, as we cannot predict all future events or conditions and as subsequent events may result in outcomes that are inconsistent with judgements that were reasonable at the time they were made, the above conclusions are not a guarantee that the Group or the Company will continue in operation.

5. Fraud and breaches of laws and regulations – ability to detect

Identifying and responding to risks of material misstatement due to fraud

To identify risks of material misstatement due to fraud ('fraud risks') we assessed events or conditions that could indicate an incentive or pressure to commit fraud or provide an opportunity to commit fraud.

Our risk assessment procedures included:

Enquiring of directors, the audit committee, internal legal counsel and inspection of policy documentation as to the Group's high-level policies and procedures to prevent and detect fraud, including the internal audit function, and the Group's channel for whistleblowing', as well as whether they have knowledge of any actual, suspected or alleged fraud.

Reading board and audit committee minutes.

Considering remuneration incentive schemes and performance targets for management, including underlying profit before tax target for management remuneration.

We communicated identified fraud risks throughout the audit team and remained alert to any indications of fraud throughout the audit. This included communication from the Group to component audit teams of relevant fraud risks identified at the Group level and request to component audit teams to report to the Group audit team any instances of fraud that could give rise to a material misstatement at a Group level.

As required by auditing standards, and taking into account possible pressures to meet profit targets, both in the current period and in future periods, we perform procedures to address the risk of management override of controls and the risk of fraudulent revenue recognition, in particular the risk that contract revenue is recognised in an overly optimistic or cautious manner given the subjective nature and risk of bias in the related accounting estimates, and the risk that Group and component management may be in a position to make inappropriate accounting entries.

We did not identify any additional fraud risks.

Further detail in respect of contract revenue is set out in the key audit matter disclosures in section 2 of this report.

We performed procedures including:

Identifying journal entries to test for all full scope components based on risk criteria and comparing the identified entries to supporting documentation. These included those posted to unusual account combinations.

Assessing significant accounting estimates for bias.

Procedures over contract revenue performed for all full scope components are detailed in section 2 of this report.

Identifying and responding to risks of material misstatement due to non-compliance with laws and regulations

We identified areas of laws and regulations that could reasonably be expected to have a material effect on the financial statements from our general commercial and sector experience, through discussion with the directors and other management (as required by auditing standards), and from inspection of the Group's regulatory and legal correspondence and discussed with the directors and other management the policies and procedures regarding compliance with laws and regulations. As the Group is regulated, our assessment of risks involved gaining an understanding of the control environment including the entity's procedures for complying with regulatory requirements.

We communicated identified laws and regulations throughout our team and remained alert to any indications of non-compliance throughout the audit. This included communication from the Group to full-scope component audit teams of relevant laws and regulations identified at the Group level, and a request for full scope component auditors to report to the Group team any instances of non-compliance with laws and regulations that could give rise to a material misstatement at Group.

The potential effect of these laws and regulations on the financial statements varies considerably. Firstly, the Group is subject to laws and regulations that directly affect the financial statements including financial reporting legislation (including related companies legislation), distributable profits legislation, taxation legislation, and pensions legislation and we assessed the extent of compliance with these laws and regulations as part of our procedures on the related financial statement items.

Secondly, the Group is subject to many other laws and regulations where the consequences of non-compliance could have a material effect on amounts or disclosures in the financial statements, for instance through the imposition of fines or litigation. We identified the following areas as those most likely to have such an effect: health and safety, anti-bribery and corruption, employment law, recognising the nature of the Group's activities. Auditing standards limit the required audit procedures to identify non-compliance with these laws and regulations to enquiry of the directors and other management and inspection of regulatory and legal correspondence, if any. Therefore, if a breach of operational regulations is not disclosed to us or evident from relevant correspondence, an audit will not detect that breach.

Context of the ability of the audit to detect fraud or breaches of law or regulation

Owing to the inherent limitations of an audit, there is an unavoidable risk that we may not have detected some material misstatements in the financial statements, even though we have properly planned and performed our audit in accordance with auditing standards. For example, the further removed non-compliance with laws and regulations is from the events and transactions reflected in the financial statements, the less likely the inherently limited procedures required by auditing standards would identify it.

In addition, as with any audit, there remained a higher risk of non-detection of fraud, as these may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal controls. Our audit procedures are designed to detect material misstatement. We are not responsible for preventing non-compliance or fraud and cannot be expected to detect non-compliance with all laws and regulations.

6. We have nothing to report on the other information in the annual report

The directors are responsible for the other information presented in the Annual Report together with the financial statements. Our opinion on the financial statements does not cover the other information and, accordingly, we do not express an audit opinion or, except as explicitly stated below, any form of assurance conclusion thereon.

Our responsibility is to read the other information and, in doing so, consider whether, based on our financial statements audit work, the information therein is materially misstated or inconsistent with the financial statements or our audit knowledge. Based solely on that work we have not identified material misstatements in the other information.

Strategic report and directors' report

Based solely on our work on the other information:

we have not identified material misstatements in the strategic report and the directors' report;

in our opinion the information given in those reports for the financial year is consistent with the financial statements; and

in our opinion those reports have been prepared in accordance with the Companies Act 2006.

Directors' remuneration report

In our opinion the part of the Directors' Remuneration Report to be audited has been properly prepared in accordance with the Companies Act 2006.

Disclosures of emerging and principal risks and longer-term viability

We are required to perform procedures to identify whether there is a material inconsistency between the directors’ disclosures in respect of emerging and principal risks and the viability statement, and the financial statements and our audit knowledge.

Based on those procedures, we have nothing material to add or draw attention to in relation to:

- the directors’ confirmation within the Viability statement that they have carried out a robust assessment of the emerging and principal risks facing the Group, including those that would threaten its business model, future performance, solvency and liquidity;

- the Emerging and Principal Risks disclosures describing these risks and how emerging risks are identified,and explaining how they are being managed and mitigated; and

- the directors’ explanation in the viability statement of how they have assessed the prospects of the Group, over what period they have done so and why they considered that period to be appropriate, and their statement as to whether they have a reasonable expectation that the Group will be able to continue in operation and meet its liabilities as they fall due over the period of their assessment, including any related disclosures drawing attention to any necessary qualifications or assumptions.

We are also required to review the viability statement, set out on Viability statement under the Listing Rules. Based on the above procedures, we have concluded that the above disclosures are materially consistent with the financial statements and our audit knowledge.

Our work is limited to assessing these matters in the context of only the knowledge acquired during our financial statements audit. As we cannot predict all future events or conditions and as subsequent events may result in outcomes that are inconsistent with judgements that were reasonable at the time they were made, the absence of anything to report on these statements is not a guarantee as to the Group’s and Company’s longer-term viability.

Corporate governance disclosures

We are required to perform procedures to identify whether there is a material inconsistency between the directors’ corporate governance disclosures and the financial statements and our audit knowledge.

Based on those procedures, we have concluded that each of the following is materially consistent with the financial statements and our audit knowledge:

- the directors’ statement that they consider that the annual report and financial statements taken as a whole is fair, balanced and understandable, and provides the information necessary for shareholders to assess the Group’s position and performance, business model and strategy;

- the section of the annual report describing the work of the Audit Committee, including the significant issues that the audit committee considered in relation to the financial statements, and how these issues were addressed; and

- the section of the annual report that describes the review of the effectiveness of the Group’s risk management and internal control systems.

We are required to review the part of the Corporate Governance Statement relating to the Group’s compliance with the provisions of the UK Corporate Governance Code specified by the Listing Rules for our review, and to report to you if a corporate governance statement has not been prepared by the Company. We have nothing to report in this respect.

Based solely on our work on the other information described above:

- with respect to the Corporate Governance Statement disclosures about internal control and risk management systems in relation to financial reporting processes and about share capital structures:

- we have not identified material misstatements therein; and

- the information therein is consistent with the financial statements; and

- in our opinion, the Corporate Governance Statement has been prepared in accordance with relevant rules of the Disclosure Guidance and Transparency Rules of the Financial Conduct Authority.

7. WE HAVE NOTHING TO REPORT ON THE OTHER MATTERS ON WHICH WE ARE REQUIRED TO REPORT BY EXCEPTION

Under the Companies Act 2006, we are required to report to you if, in our opinion:

- adequate accounting records have not been kept by the parent Company, or returns adequate for our audit have not been received from branches not visited by us; or

- the parent Company financial statements and the part of the Directors’ Remuneration Report to be audited are not in agreement with the accounting records and returns; or

- certain disclosures of directors’ remuneration specified by law are not made; or

- we have not received all the information and explanations we require for our audit.

We have nothing to report in these respects.

8. RESPECTIVE RESPONSIBILITIES

Directors’ responsibilities

As explained more fully in their statement set out in Statement of directors' responsibilities, the directors are responsible for: the preparation of the financial statements including being satisfied that they give a true and fair view; such internal control as they determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error; assessing the Group and parent Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern; and using the going concern basis of accounting unless they either intend to liquidate the Group or the parent Company or to cease operations, or have no realistic alternative but to do so.

Auditor’s responsibilities

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue our opinion in an auditor’s report. Reasonable assurance is a high level of assurance, but does not guarantee that an audit conducted in accordance with ISAs (UK) will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of the financial statements.

A fuller description of our responsibilities is provided on the FRC’s website at www.frc.org.uk/auditorsresponsibilities.

The Company is required to include these financial statements in an annual financial report prepared using the single electronic reporting format specified in the TD ESEF Regulation. This auditor’s report provides no assurance over whether the annual financial report has been prepared in accordance with that format.

9. THE PURPOSE OF OUR AUDIT WORK AND TO WHOM WE OWE OUR RESPONSIBILITIES

This report is made solely to the Company’s members, as a body, in accordance with Chapter 3 of Part 16 of the Companies Act 2006. Our audit work has been undertaken so that we might state to the Company’s members those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Company and the Company’s members, as a body, for our audit work, for this report, or for the opinions we have formed.

Craig Parkin (Senior Statutory Auditor) for and on behalf of KPMG LLP, Statutory Auditor

Chartered Accountants

One Sovereign Square

Sovereign Street

Leeds

LS1 4DA

14 June 2023